Email: hamish@transparently.ai

A cyanide-toting spy from the Cold War would probably find the current frosting between China and the US diverting. It is difficult to judge the more farcical: the US reaction to spy balloons or China’s fear of Big 4 auditors.

You probably heard that several Chinese authorities, including the Ministry of Finance, have urged state-owned firms to phase out using the Big 4 due to concerns about data security. State-owned firms will replace the Big 4 with Chinese or Hong Kong auditors as their contracts expire.

Leaving aside the question as to whether the Big 4 are more or less likely to harbour spies than a nondescript Hong Kong auditor, we suspect this move will do more harm than good.

It is no secret that Chinese SOEs are unloved by investors and trade at a discount to the broader stock market. For the most part this is due to low profitability and concerns about governance.

What will ditching the Big 4 do?

Academic research supports the proposition that Big 4 auditors improve audit quality. Efforts to quantify the effect, however, have thus far proven elusive.

Big 4 auditors improve audit quality.

Enter CASPER, our AI accounting risk measurement platform. CASPER is able to quantify the difference in accounting manipulation risk between firms with a Big 4 auditor and those without.

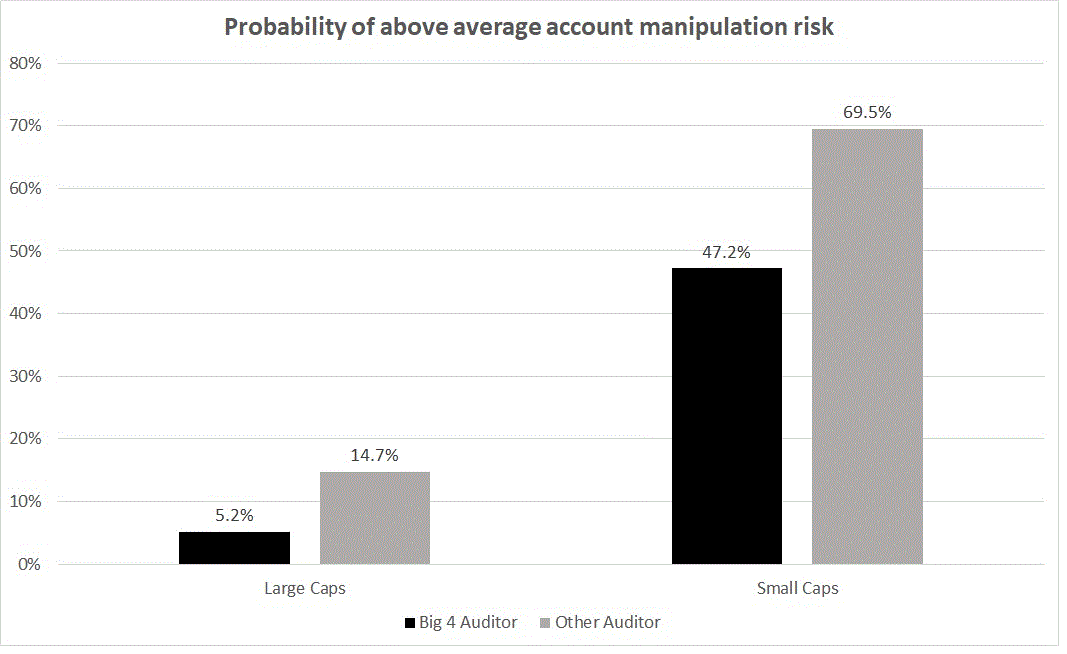

For large cap firms, the probability of above-average account manipulation rises from 5.2% for firms with a Big 4 auditor to 14.7% for firms without.

…the risk of above average account manipulation is roughly three times higher for large firms without a Big 4 auditor.

In other words, we can say that the risk of above average account manipulation is roughly three times higher for large firms without a Big 4 auditor than for firms with a Big 4 auditor.

In the small caps, the probability of above average account manipulation rises from 47.2% to 69.5%.

Put another way, the probability of above average account manipulation rises 22.3% when a small company does not have a Big 4 auditor.

These risk increases are significant and represent a significant downgrade in account quality for firms lacking a Big 4 auditor. Little wonder that many investors avoid companies without a Big 4 auditor, especially in the small caps.